Leased vs. Owned FLNG/FPSO Units: Financial Implications and Strategic Trade-offs

In the offshore oil and gas industry, the decision to lease or own a floating production unit such as an FPSO (Floating Production Storage and Offloading) or FLNG (Floating Liquefied Natural Gas) vessel carries significant financial and strategic implications. This article explores the key differences between leased-operated vessels and those owned directly by oil companies, focusing on financial structures, risk allocation, long-term flexibility, and hybrid ownership models.

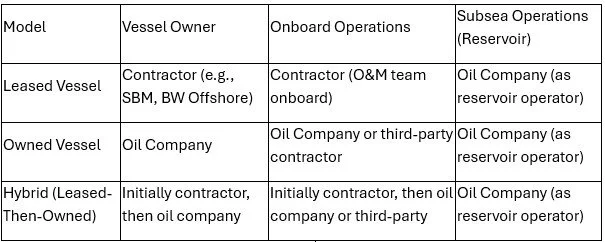

Ownership and Operational Responsibility Matrix

In both models, the oil company retains responsibility for subsea operations, including reservoir management, well intervention, and flow assurance. This is due to their role as the field operator, which includes regulatory accountability and production optimization. Onboard operations, however, differ significantly: leased vessels are typically operated by the contractor, while owned vessels may be operated directly by the oil company or outsourced to a specialized O&M provider. Hybrid models begin with contractor-led operations and transition to company-led control upon transfer of ownership.

CAPEX vs. OPEX Structure

Leased Vessel:

Requires minimal upfront capital investment from the oil company.

Payments are made as lease fees, typically categorized as operating expenses (OPEX).

Suitable for marginal fields or when capital preservation is a priority.

Especially valuable when the production lifetime of the field is shorter than the vessel’s design life (typically 20–30 years), allowing reuse or redeployment.

Owned Vessel:

Demands substantial upfront capital expenditure (CAPEX).

The vessel becomes a long-term asset on the company’s balance sheet.

Potentially lower lifecycle costs if reused across multiple projects.

Makes more sense when the field’s production lifetime matches or exceeds the vessel’s design life, ensuring full utilization of the asset and maximizing return on investment over its design life.

Balance Sheet and Financial Metrics

Leased Vessel:

May be treated as off-balance sheet (though IFRS 16 and ASC 842 now require lease liabilities to be recognized).

Enhances return on capital employed (ROCE) by reducing asset base.

Attractive for companies seeking asset-light strategies.

Allows oil companies with large reserves (e.g., Petrobras) to accelerate production volumes without significantly increasing reported debt, preserving financial flexibility.

Owned Vessel:

Full asset and depreciation are recorded on the balance sheet.

Higher asset base can dilute ROCE unless production volumes are high.

Offers greater control but increases financial exposure.

Accounting Sidebar: IFRS 16 & ASC 842

IFRS 16 (International Financial Reporting Standards) and ASC 842 (U.S. GAAP) are lease accounting standards that require companies to recognize most leases on their balance sheets. Under these rules:

Lessees must record a right-of-use asset and a lease liability for long-term leases.

This increases transparency and comparability in financial reporting.

Previously, operating leases could be kept off-balance sheet; now, they impact debt ratios and asset base.

For FPSO/FLNG leases, this means oil companies must account for the financial impact of vessel leases more explicitly, influencing decisions on leasing vs. owning.

Risk Allocation

Leased Vessel:

Construction, commissioning, and operational risks are largely borne by the contractor.

Oil company benefits from performance guarantees and uptime clauses.

Contractor assumes responsibility for technical failures and delays.

Owned Vessel:

Oil company bears full lifecycle risk.

Requires internal or third-party expertise for operations and maintenance.

Greater exposure to market volatility and execution risks.

Flexibility and Redeployment

Leased Vessel:

Easier to redeploy or terminate contract if field economics change.

Ideal for short-cycle or exploratory developments.

Owned Vessel:

Less flexible; redeployment involves significant planning and cost.

Better suited for long-term, high-volume fields.

Strategic Control

Leased Vessel:

Limited control over vessel design and operational decisions.

Dependency on contractor’s capabilities and priorities.

Owned Vessel:

Full control over design, integration, and upgrades.

Easier alignment with company-specific standards and digitalization strategies.

Tax and Accounting Considerations

Lease payments may be tax-deductible as operating expenses.

Owned assets benefit from depreciation and investment allowances.

Jurisdictional factors (e.g., PSC terms, local content rules) influence the optimal model.

Hybrid Models: Leased-Then-Owned (Transfer Options)

Some oil companies adopt a hybrid strategy, leasing a vessel for the initial years of production and then exercising a purchase option to take ownership. This model combines the financial flexibility of leasing with the long-term control of ownership.

Example: FPSO Liza Destiny (ExxonMobil)

Initially leased from SBM Offshore under a long-term charter.

ExxonMobil retained the option to purchase the unit after a defined period.

This approach allowed ExxonMobil to mitigate early-stage risks while securing long-term asset control.

Advantages of Transfer Options:

Reduces upfront CAPEX while preserving future ownership rights.

Allows performance validation before committing to full ownership.

Can be structured to optimize tax and depreciation benefits.

Case Insight: SBM Offshore and Petrobras – Alexandre de Gusmao FPSO

A recent example of a long-term lease contract is the Alexandre de Gusmao FPSO, operated by SBM Offshore for Petrobras in Brazil’s Mero pre-salt field. The vessel arrived in early 2025 and is expected to begin operations between Q2 and Q3 of the year. The contract spans 22.5 years, covering both charter and operational services.

Key Highlights:

Production capacity: 180,000 barrels/day of oil and 12 million cubic metres/day of gas.

Supports 15 development wells, including oil producers and gas injectors.

Will increase Mero’s processing capacity by 31% to 770,000 bpd.

All associated gas will be reinjected to enhance productivity.

This case underscores the strategic value of long-term leasing in high-capacity fields, allowing Petrobras to scale production while leveraging SBM’s operational expertise and Fast4Ward hull design.

Conclusion

The choice between leasing and owning an FPSO or FLNG unit is not merely financial—it reflects a company’s broader strategic posture, risk appetite, and operational philosophy. Leased vessels offer flexibility and reduced upfront costs, while owned units provide control and potential long-term savings. Hybrid models, such as lease-to-own arrangements, offer a compelling middle ground for companies seeking both agility and asset control.

Floaters Intelligentia continues to explore these dynamics to support smarter, more agile decision-making in the floating production sector.

APA Reference:

SBM Offshore. (2025, May 27). FPSO Alexandre de Gusmão producing and on hire. Retrieved from https://www.sbmoffshore.com/newsroom/fpso-alexandre-de-gusmao-producing-and-on-hire/ [sbmoffshore.com]