LNG Liquefaction Technologies in Modern FLNG Projects

Floating LNG (FLNG) has entered a new phase of maturity, driven by rapid advances in liquefaction technologies and the emergence of multiple equipment suppliers capable of supporting offshore modular LNG production. Over the last decade, the LNG industry has diversified from a duopoly of large coil‑wound heat exchanger (CWHE) manufacturers into a broader ecosystem where mixed‑refrigerant cycles, brazed‑aluminum heat exchangers, and fully modular trains play an increasingly important role in enabling mid‑scale FLNG deployments.

At the core of all liquefaction technologies—regardless of scale or process configuration—sits the cryogenic heat exchanger, the item responsible for removing heat from the natural gas stream and turning it into LNG. Whether implemented as a single large coil‑wound exchanger or as multiple plate‑fin exchangers arranged in parallel inside a cold box, this equipment represents the thermodynamic heart of the LNG train.

From a conceptual standpoint, the Main Cryogenic Heat Exchanger (MCHE) can be likened to the evaporator of a household refrigerator or air‑conditioning system. In both cases, a refrigerant absorbs heat from a warmer stream and evaporates at low temperature, providing cooling. The analogy, however, rapidly breaks down when scale and operating conditions are considered.

While a domestic evaporator cools air by a few tens of degrees, the MCHE must cool and liquefy natural gas down to approximately −160 °C, handling multiple process and refrigerant streams, very high mass flowrates, and near‑continuous operation. In doing so, the MCHE concentrates within a single item of equipment the thermodynamic core of the entire liquefaction process. For this reason, it is commonly described as the “heart” of an LNG train: when the MCHE is unavailable, LNG production stops entirely.

This central role also makes the MCHE one of the most critical and vulnerable pieces of equipment in any LNG facility. Damage, severe fouling, or loss of integrity in the main cryogenic exchanger results in an immediate train shutdown and, in many cases, a prolonged loss of capacity.

This vulnerability was starkly demonstrated in March 2026, when missile attacks on Qatar’s Ras Laffan Industrial City damaged two LNG trains (Train 4 and Train 6), temporarily removing approximately 17% of Qatar’s LNG liquefaction capacity from the global market. Official statements from QatarEnergy confirmed that the damage was concentrated in the liquefaction section, with extensive destruction of the cold end of the process. Independent assessments and satellite imagery indicate that the damage likely affected the main cryogenic heat exchangers and associated cold box structures, which form the core of both AP‑C3MR and AP‑X liquefaction technologies used at Ras Laffan. As a consequence, QatarEnergy indicated that repairs could require three to five years, an exceptionally long outage by LNG industry standards.

The expected duration of the outage is directly linked to another defining characteristic of MCHEs: their extremely long delivery time. Main cryogenic heat exchangers are custom‑engineered, one‑off items, designed specifically for each LNG train’s capacity, refrigerant cycle, and process configuration. They are typically manufactured in aluminum alloys, particularly for coil‑wound and plate‑fin designs, due to aluminum’s excellent thermal conductivity and favorable mechanical behavior at cryogenic temperatures. In some auxiliary or niche applications, cryogenic stainless steels may also be used.

Manufacturing MCHEs involves highly specialized fabrication techniques, including precision tube winding or vacuum brazing, and is limited to a very small number of qualified suppliers worldwide. As a result, MCHEs are among the longest‑lead items in an LNG project. For large onshore or offshore LNG trains, typical delivery times range from 30 to 36 months, and in the case of unplanned replacement following damage, lead times can extend even further due to order backlogs and the non‑standard nature of the equipment.

The Qatar case therefore illustrates a broader and structural reality of LNG technology: damage to the cryogenic heat exchangers does not merely cause an operational upset, but creates a multi‑year loss of capacity, even for the world’s most capital‑rich and technically advanced operator. This combination of process centrality, limited manufacturability, and long replacement timelines makes the MCHE not only the technical heart of the LNG train, but also one of its most strategically sensitive assets.

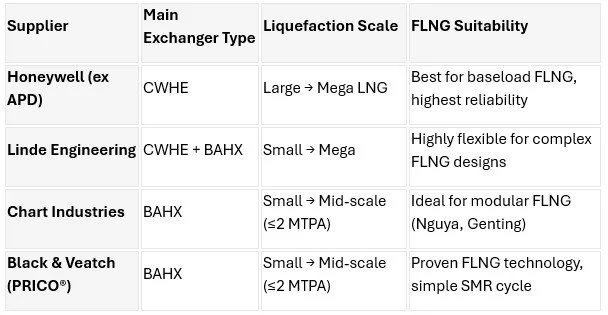

This article provides a comparative technical overview of the four dominant players influencing today’s FLNG liquefaction landscape: Honeywell (formerly Air Products LNG business), Linde Engineering, Chart Industries, and Black & Veatch (PRICO®).

Honeywell (ex Air Products): The Global Leader in Coil‑Wound Heat Exchangers

Honeywell became the world’s leading provider of LNG liquefaction technology in 2024 after acquiring Air Products’ entire LNG process technology and equipment business. Following the acquisition, Honeywell now controls the industry's most established portfolio of coil‑wound heat exchangers (CWHE), widely considered the gold standard for large‑scale and robust offshore liquefaction systems.

Honeywell explicitly states that it is “the world’s leading provider of natural gas liquefaction technology, coil‑wound heat exchangers and related equipment”, with more than 120 LNG plants designed and commissioned worldwide.

CWHEs offer high throughput in a compact vertical arrangement with exceptional reliability, making them the preferred choice for baseload LNG plants and large‑scale FLNG units. Their ability to handle multi‑stream flows, tolerate large thermal gradients, and operate under challenging offshore conditions remains unmatched.

Key strengths for FLNG:

Highest capacity per exchanger, suitable for >3–6 MTPA per train

Robust mechanical integrity under vessel motions

Long track record in harsh environments

Fully integrated with Honeywell’s digital automation suite (Forge & Experion)

Honeywell remains the principal supplier for any operator seeking world‑scale or mega‑FLNG liquefaction reliability.

AirProducts’ MCHE. Source: AirProducts

Linde Engineering: The Only Supplier Offering Both CWHE and Plate‑Fin Heat Exchangers

Linde Engineering occupies a unique position in the LNG industry: it is the only equipment manufacturer capable of producing both coil‑wound heat exchangers and plate‑fin (brazed aluminum) heat exchangers, providing complete coverage from small‑scale modular solutions to world‑scale LNG plants.

Linde has delivered over 30 LNG plants globally since 1967, using a portfolio of proprietary liquefaction processes ranging from 10,000 tpa to over 10 MTPA. Their coil‑wound units directly compete with Honeywell’s for large‑scale plants, while their plate‑fin units serve modular or mid‑scale applications.

Key strengths for FLNG:

Dual‑technology flexibility (CWHE + plate‑fin)

Strong experience with nitrogen rejection and complex feed gas compositions

Proven global EPC and modularization capability

For operators needing hybrid process designs or integrated NGL/LNG recovery on FLNG, Linde remains the most flexible and technically diverse supplier.

Chart Industries: The Leading Supplier of Brazed Aluminum Heat Exchangers and Cold Boxes

Chart Industries is not a CWHE manufacturer, but it is the world’s leading producer of brazed‑aluminum heat exchangers (BAHX) and fully integrated cold boxes—equipment that forms the core of many small and mid‑scale LNG liquefaction processes.

Chart BAHX units are “at the heart of cryogenic separation, liquefaction and purification processes,” including LNG liquefaction. Chart’s expertise is reinforced by decades of innovation, including vacuum brazing, mercury‑tolerant designs, and modular cold box fabrication.

While BAHX are not used as main exchangers in baseload LNG plants, they play a crucial role in recent mid-scale FLNG units, where small footprint, modularity, and weight reduction are top priorities. This includes projects such as Nguya FLNG and Genting FLNG, developed with modular process philosophies consistent with Chart’s equipment offering (even though the vendors are not named explicitly in public documents).

Key strengths for FLNG:

Highly compact and lightweight design ideal for topside modules

Excellent multi‑stream heat transfer efficiency

Cost‑effective compared to CWHEs

Strong synergy with modular mid‑scale liquefaction cycles (e.g., IPSMR®)

Chart is therefore essential when discussing FLNG solutions under ~1–2 MTPA per train.

Chart’s BAHX. Source: Chart

Black & Veatch: PRICO® SMR and Plate‑Fin Heat Exchangers for FLNG

Black & Veatch delivers its proprietary PRICO® LNG process, based on a Single Mixed Refrigerant (SMR) cycle, which is widely used in modular and floating LNG applications. The company notes that PRICO® has been deployed in “dozens of onshore and nearly half of the floating plants in operation globally,” and remains a cornerstone of their FLNG offerings.

Technically, PRICO® relies on plate‑fin brazed aluminium heat exchangers (BAHX) arranged in parallel within a cold box—making it fundamentally different from CWHE‑based baseload designs. The refrigerant heat exchanger in PRICO consists of “multiple plate-fin brazed aluminum cores arranged in parallel”.

PRICO® was also the first liquefaction technology to produce LNG on a floating facility (2016), demonstrating its robustness and simplicity offshore. Recent collaborations combine PRICO with high‑efficiency Baker Hughes LM9000 turbomachinery for mid‑scale FLNG up to 2 MTPA per train.

Key strengths for FLNG:

Extremely compact system tailored for modular FLNG

Simple SMR loop reduces complexity and OPEX

High suitability for remote or redevelopment projects

Proven deployment success on floating assets

Black & Veatch therefore anchors the mid‑scale FLNG segment alongside Chart.

Comparative Summary: Which Technology Fits Which FLNG Class?

Conclusion

The landscape of LNG liquefaction technologies for FLNG applications is inherently constrained—not only by offshore integration limits, but also by the very small and highly specialized market for main cryogenic heat exchangers (MCHEs). Only a limited number of suppliers worldwide are capable of designing and manufacturing MCHEs suitable for FLNG service, and their production capacity is constrained by bespoke engineering, specialized fabrication processes, and stringent quality requirements.

Compounding this limitation, MCHEs are among the longest‑lead items in an FLNG project, with typical delivery times extending to 30–36 months or more, particularly for large coil‑wound exchangers. As demonstrated by recent events in Qatar, damage to the cryogenic core of an LNG train can translate into multi‑year loss of capacity, even for the world’s most established LNG operators. This reality underscores the strategic weight carried by the choice of liquefaction technology.

As a consequence, the selection of the liquefaction process—and by extension the type of cryogenic heat exchanger—is not merely a downstream engineering decision, but one of the earliest and most critical choices to be taken during FLNG project development. Once made, this decision effectively locks in key aspects of the project, including schedule, execution risk profile, vendor dependence, modularization strategy, and long‑term operability.

Against this background, the market is clearly segmenting into two parallel tracks:

High‑capacity, baseload FLNG — relying on CWHE technologies from Honeywell and Linde, offering unparalleled reliability and throughput.

Mid‑scale, modular FLNG — driven by Chart Industries’ plate‑fin exchangers and Black & Veatch’s PRICO® SMR process, enabling fast‑track, relocatable, and cost‑efficient floating LNG solutions.

In this context, a deep understanding of the strengths, limitations, and operational implications of each MCHE technology—coil‑wound versus plate‑fin, large single‑train versus modular parallel concepts—is of paramount importance. Such understanding is essential not only to optimize performance and footprint, but also to manage execution risk and ensure the resilience of future FLNG developments in an increasingly tight and geopolitically exposed LNG supply chain.

References

Air Products and Chemicals, Inc. (2018). Liquefied natural gas technology: Main cryogenic heat exchangers for LNG plants. Air Products. https://www.airproducts.com

Black & Veatch. (2023). PRICO® liquefaction process for LNG and FLNG applications. Black & Veatch Corporation. https://www.bv.com

Chart Industries. (2022). Brazed aluminum heat exchangers for LNG applications. Chart Industries. https://www.chartindustries.com

Honeywell. (2024). Honeywell completes acquisition of Air Products’ LNG process technology and equipment business. Honeywell Press Release. https://www.honeywell.com

Linde Engineering. (2021). LNG liquefaction technologies and main cryogenic heat exchanger solutions. Linde plc. https://www.linde-engineering.com

QatarEnergy. (2026, March 19). QatarEnergy statement on missile attacks on its LNG facilities. https://www.qatarenergy.qa

Reuters. (2026, March 19). Iranian attacks damage Qatar LNG trains, taking 17% of capacity offline. Reuters. https://www.reuters.com

Touil, M. (2026, March 26). Has QatarEnergy lost 17% of its liquefaction capacity? Look again. LinkedIn. https://www.linkedin.com

Ullmann, H., & Kockelmann, H. (2017). Cryogenic plate‑fin and coil‑wound heat exchangers in LNG service. Heat Transfer Engineering, 38(13–14), 1131–1145. https://doi.org/10.1080/01457632.2017.1305692

Zeeshan, A., & Manikandan, A. (2017). Failure caused by mercury embrittlement in a main cryogenic heat exchanger in an LNG plant. SPE Abu Dhabi International Petroleum Exhibition & Conference. https://doi.org/10.2118/188608-MS