Construction All Risks Insurance in Offshore Projects: Policy Architecture, Thresholds, Limits & Marine Warranty Surveyor Involvement

Construction All Risks (CAR) insurance underpins risk transfer and governance on major offshore projects—FPSOs, FLNGs, and complex subsea campaigns. Well-structured CAR programs do more than pay claims: they shape behavior by requiring method statements, marine operations approval, and readiness gates before the riskiest activities (heavy lifts, long-haul tows, offshore installation) commence. This article sets out a practitioner’s guide to policy architecture, generic limit and deductible structures, and when Marine Warranty Surveyors (MWS) must be involved. A particular focus is the often-missed threshold rule: the contractor’s CAR usually carries a relatively modest fixed limit for yard-centric operations; above that threshold, the owner’s CAR must engage—sometimes even for lifts performed at the yard when the item value exceeds the contractor’s limit. We close with practical integration steps, a diagram that visualizes the coverage handover by value threshold, and a checklist to keep approvals aligned with the schedule.

What CAR Insurance Covers and Why Offshore Projects Rely on It

A CAR program protects works, materials, equipment, and temporary works against physical loss or damage during construction, load-out, transit, installation, and (often) hook-up and commissioning. It typically includes reasonable expenses to protect insured property after an incident (sue and labor), removal of wreckage or debris, specified testing/trials, and may package third‑party legal and contractual liability alongside material damage to create a single execution framework.

Offshore construction is characterized by high value-at-risk and non‑routine operations: quay‑side heavy lifts of modules; sea‑fastening and barge transports; wet/dry tows of hulls or floating units over long routes; and offshore installation of moorings, turrets, risers, and subsea structures. Because these operations are episodic and mission‑critical, even small preparation defects or weather deviations can cause outsized loss and delay. The insurance therefore acts as both financial transfer and behavioral contract, embedding prerequisites and independent verification to reduce risk to acceptable levels before gates are crossed.

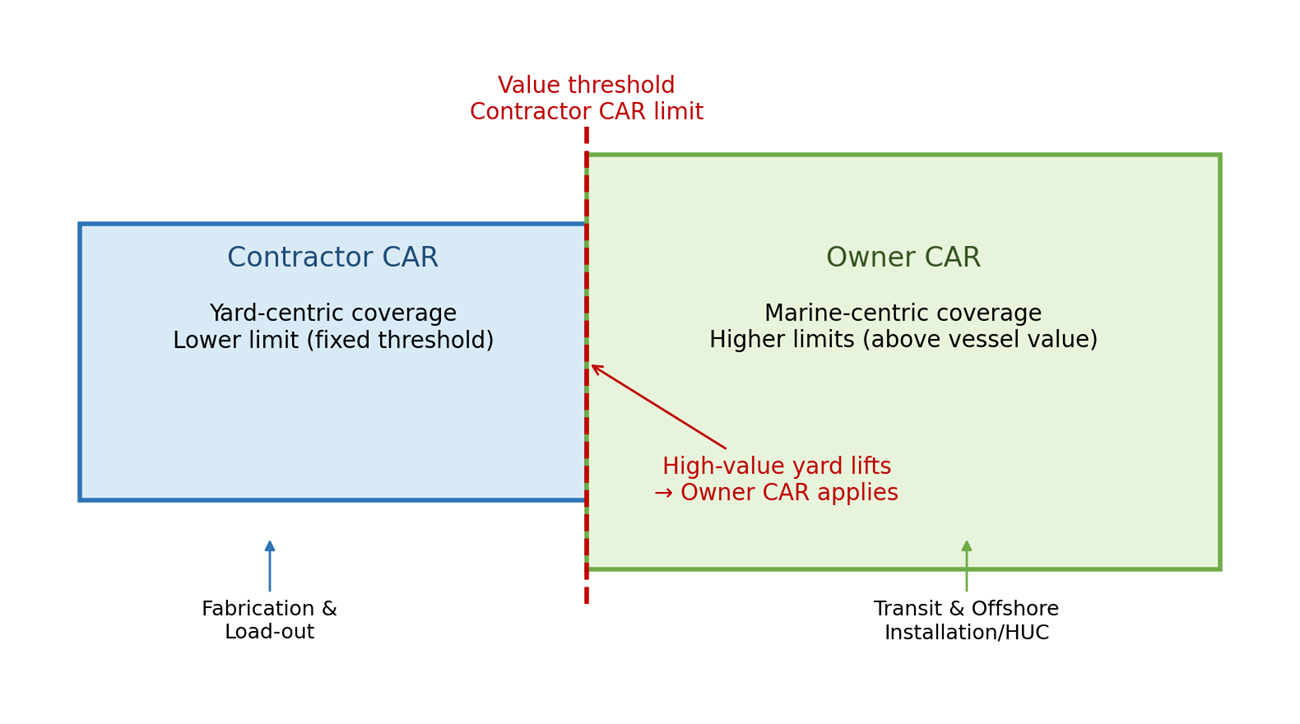

Policy Architecture and the Threshold Rule: Contractor CAR vs Owner CAR

Most floating production projects implement complementary placements that dovetail at a clear boundary of custody and control and, critically, at a value threshold.

Contractor’s CAR (yard‑centric): This placement covers fabrication yards, assembly areas, temporary works, inland transit, and port operations up to load‑out and sea‑fastening. It is designed for attritional and moderate‑severity risks and is typically written with a fixed limit that reflects yard exposures. When the declared value of a single item or lift exceeds that fixed limit the contractor’s placement cannot—by design—carry the loss.

Owner’s CAR (marine‑centric, higher limits): This placement addresses high‑severity exposures from long‑haul transit and offshore operations (tow, installation, hook‑up, commissioning) and is configured with much higher limits, often set above the vessel’s insured value to capture catastrophic scenarios during marine operations. Importantly, the owner’s CAR also engages for high‑value yard lifts when the item value crosses the contractor’s threshold, even if the operation occurs within the yard.

This approach is consistent with industry guidance such as JR2019-006 and JR2019-006a, which emphasize explicit threshold governance to prevent coverage gaps and ensure seamless transition between contractor and owner CAR placements.

Boundary and handover: In addition to the custody/operations handover (e.g., ‘hook of the crane’ or documented transfer to the marine spread), project teams must implement the value threshold handover. This ensures that coverage moves to the owner’s CAR whenever the itemized value of a yard activity exceeds the contractor’s limit, avoiding gaps and disputes after an incident.

Contracting and governance: Reflect the threshold rule explicitly in EPC and logistics contracts, define who initiates owner‑CAR coverage for high‑value yard lifts, and maintain a live threshold check in the lifting plan approval workflow.

Practical example: A compressor module is lifted at the yard. If the module’s declared value is below the contractor’s CAR limit, the lift proceeds under the contractor’s placement. If the value is above the contractor’s limit, the lift must be insured under the owner’s placement—even though the location and operation are yard‑based.

Coverage split by value threshold (generic)

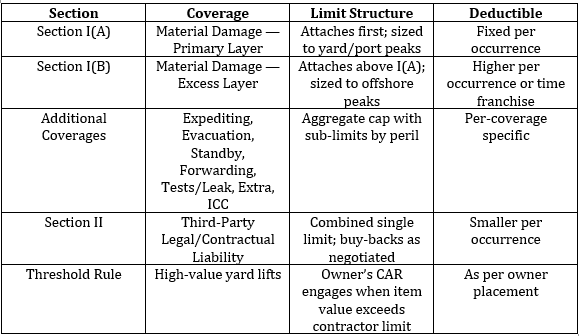

Generic Limit Structures, Additional Coverages, and Deductibles (No Numbers)

Material damage is often structured in layers: a primary layer (Section I(A)) sized to yard/port exposures and one or more excess layers (Section I(B)) aimed at peak exposures during offshore installation and critical heavy‑lift phases. Additional coverages are commonly aggregated under an overall cap with sub‑limits by peril—expediting expenses, evacuation expenses, standby charges, forwarding charges, tests/leak search, extra expenses, and increased cost of construction mandated by regulation.

Deductibles follow operational reality: fixed deductibles per occurrence in the yard; higher deductibles or time franchises for marine spread standby; smaller deductibles for third‑party liability with clear wording around existing property, contractual assumptions of liability, and negotiated buy‑backs.

Escalation and value reconciliation: Because declared schedules evolve, programs typically include a process that reconciles provisional values to completed values, automatically accepting increases (with premium adjustment) and capping recovery relative to the latest declared schedule to avoid over‑insurance and administrative churn.

Governance artefacts: Maintain a register of warranted operations and align it with the limit map, deductibles, and the threshold rule so decision‑makers understand both technical preconditions and insurance consequences.

Visual Summary — CAR Policy Limits and Deductibles

Marine Warranty Surveyor (MWS): Role, Triggers, COA as Condition Precedent

Warranty endorsements for upstream construction formalize the MWS role and make a Certificate of Approval (COA) a condition precedent to coverage for defined critical operations. The MWS reviews procedures, vessel capability, rigging plans, sea‑fastening design, metocean criteria, and contingencies, and issues a COA when satisfied that risk is reduced to acceptable levels.

As reinforced in JR2019-006a, COA issuance is a critical prerequisite for coverage of high-risk marine operations, underscoring the need for strict compliance with approved procedures.

Why Management of Change (MoC) Matters:

Any change to an approved method statement, rigging plan, or tow configuration must trigger a formal MoC process and re-engagement with the MWS. If a change is implemented without MWS review and updated COA, coverage for that operation can be denied—even if the original plan was approved. This is because the insurer’s warranty endorsement ties coverage to compliance with the approved procedure.

Typical Triggers for MWS and MoC:

Yard load-outs and heavy lifts

Sea-fastening verification

Long-haul tows

Offshore installation of turrets, moorings, risers, and subsea structures

Competence and accreditation

Approved firms typically include established global warranty surveyors (e.g., Matthews Daniel, Bureau Veritas, DNV, LOC, Global Maritime, Sterling Technical). Agree a Project‑Specific Scope of Work (PSSOW) early and define lines of communication among assured parties, broker, lead underwriter, and MWS team to avoid late‑cycle delays.

Controls and visibility

Embed COA milestones in the readiness dashboard (planned, under review, issued). Deviation from approved procedures must trigger re‑review and updated COA to preserve coverage.

Embed MoC checkpoints in the readiness dashboard and lifting/towing workflow. Ensure deviations are logged, reviewed, and approved by the MWS before execution. Failure to do so can result in a breach of warranty and rejection of claims.

MWS Endorsement — Callout (Generic)

Independent MWS approval required for critical marine operations.

COA is a condition precedent to coverage for warranted operations.

PSSOW to be agreed promptly; a generic scope applies until agreed.

Approved firms commonly include Matthews Daniel, Bureau Veritas, DNV, LOC, Global Maritime, Sterling Technical.

Method deviations require re‑review and updated COA.

How to Make CAR and MWS Work for the Project

Integrate insurance with engineering and logistics: map warranties and COA gates to method statements and the project schedule; confirm MWS deliverables in EPC and marine spread contracts; and track COA issuance against sail‑away and lift windows to avoid last‑minute slippage.

Implement the threshold check: For every significant yard lift, include a documented step where the item value is checked against the contractor’s CAR limit. If it exceeds that limit, switch coverage to the owner’s CAR and record the decision in the lifting plan package.

Administrative hygiene: Keep endorsements and schedules consistent across placements, align waiver‑of‑subrogation language with multi‑assured structures, and address existing property exclusions and buy‑backs for proximity and tie‑in agreements. Maintain consolidated files of handovers, survey reports, COAs, and notifications so a claim can be executed efficiently if needed.

Common pitfalls: ambiguous boundaries between placements; missing or outdated MWS SOW; method deviations without re‑approval; misaligned deductibles that confuse repair responsibility; and failure to update value declarations—leading to caps that limit recovery. A monthly governance session with insurance, engineering, logistics, and MWS present reduces these risks.

Checklist — Keeping Thresholds and Approvals on Track

Identify the contractor’s CAR fixed limit and publish it in lifting governance.

Require an item value declaration for every significant lift; perform the threshold check.

If threshold exceeded, trigger owner’s CAR coverage and record the decision in the lift file.

Map COA milestones to lift/transit/install dates; track status weekly.

Keep endorsements, buy‑backs, and waivers consistent across both placements.

Maintain a register of warranted operations aligned to method statements and risk reviews.

Reconcile declared values monthly, update schedules for escalation and premium adjustment.

Refer to JR2019-006 for detailed threshold management protocols and JR2019-006a for best practices in MWS governance and COA integration.

Conclusion

Offshore construction success depends on aligning technical excellence with disciplined risk governance. The contractor/owner split is not only about operational custody; it is also about value thresholds that determine when coverage must step up from modest yard limits to higher owner limits—even inside the yard—so catastrophic exposures are properly insured. By embedding threshold checks, COA gating, and clear handovers into the project’s routine, CAR becomes a framework for readiness: the right approvals at the right time, the right limits for the right operations, and auditable governance that lenders and insurers can trust.

References:

JR2019-006: Offshore Construction CAR Threshold Governance Guidelines

JR2019-006a: Marine Warranty Surveyor Endorsement and COA Compliance Framework