Asia’s Offshore Giants: Comparing Chinese and South Korean Shipyards in FPSO and FLNG Construction. 1st part: track record

As the global energy industry pivots toward offshore production and liquefied natural gas (LNG), two Asian powerhouses—China and South Korea—are competing for dominance in the construction of Floating Production Storage and Offloading (FPSO) units and Floating Liquefied Natural Gas (FLNG) facilities. While both nations boast formidable shipbuilding industries, their strengths, strategies, and global reputations diverge significantly.

This article wants to take into consideration only major yard that can handle all FPSO/FLNG fabrication and integration activities.

China: Scale, Speed, and State Support

China’s shipbuilding sector, led by state-owned conglomerates like China State Shipbuilding Corporation (CSSC), has grown into the world’s largest by volume. With facilities such as Shanghai Waigaoqiao Shipbuilding (SWS) and Dalian Shipbuilding Industry Company (DSIC), China is rapidly expanding its offshore capabilities.

Production Capacity: China commands over 50% of global shipbuilding output, giving it unmatched scale.

Cost Advantage: Lower labor and material costs make Chinese yards highly competitive on price.

State-Driven Expansion: Government backing fuels rapid development and integration with national energy firms.

However, China still lags in FLNG technology maturity, with fewer completed projects and limited experience in high-complexity offshore engineering.

South Korea: Precision, Prestige, and Proven Performance

South Korea’s shipyards—Hyundai Heavy Industries (HHI), Samsung Heavy Industries (SHI), and Hanwha Ocean (formerly DSME)—are globally recognized for their technological sophistication and reliability.

FLNG Leadership: Korea built the world’s first FLNG vessel, Prelude, for Shell.

Global Clientele: Korean yards are the preferred choice for oil majors due to their track record and quality.

Engineering Excellence: Decades of experience in FPSO and LNG vessel construction.

The trade-off? Higher costs and a smaller production base compared to China.

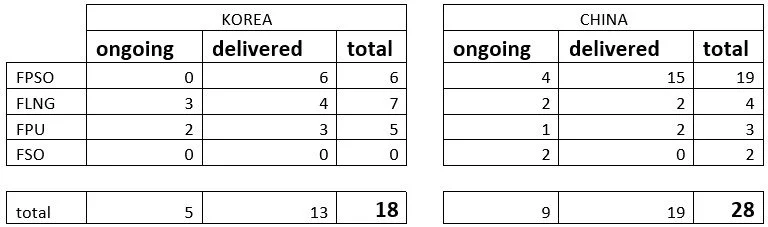

Track Record: Who Has Built What?

Past performance is one of the most reliable indicators of future success in offshore construction. South Korea continues to set the standard in FLNG, driven by engineering excellence and integrated heavy-lift capabilities. Meanwhile, China is diversifying aggressively—adding FPSO, FLNG, FPU, and FSO projects to its portfolio—while Cosco Group’s multi-yard strategy signals its ambition to become a full-spectrum offshore construction powerhouse

FPSO Construction

🇰🇷 South Korea South Korean shipyards have delivered or are currently building over 30 FPSO units, cementing their reputation as global leaders. Key players include:

Samsung Heavy Industries (SHI): Delivered major projects such as Egina (2018, TotalEnergies) and Reliance FPSO (2022, Reliance Industries)

Hyundai Heavy Industries (HHI): Known for Goliat (2015, Eni) and Glen Lyon (2016, BP).

Hanwha Ocean (formerly DSME): Delivered Ichthys FPSO (2017, Inpex) and P-79 FPSO (2026, Petrobras).

🇨🇳 China Chinese yards have built or are building at least 15 FPSO units, often in collaboration with international operators:

COOEC: Delivered P-67 (2018, Petrobras), Liuhua 16-2 FPSO (2020, CNOOC), Penguin FPSO (2022, Shell) and Haikui No. 1 (2024, CNOOC).

COSCO Qidong: delivered Western Island FPSO (2017, Dana Petroleum), Tortue FPSO (2023, BP) and is building Raia FPSO (Modec-Equinor) and Gran Morgu FPSO (SBM-TotalEnergies).

COSCO Shanghai: delivered Agogo FPSO (2025, Yinson-Azule), Maria QuiteriaFPSO (2024, Yinson-Petrobras) and Anna Nery (2022, Yinson-Petrobras).

COSCO Dalian: delivered P-77 FPSO (2018, Petrobras), and is building Gato de Mato FPSO (Modec-Shell) and refurbishing BW Maromba FPSO (BW Energy).

CIMC Raffles: Delivered Mero 3 (2024, Petrobras).

CMHI: delivered Hai Yang Shi You (Lufeng) 123 FPSO (2023, CNOOC)

🛠️ Note: Both Korean and Chinese shipyards have also contributed to partial FPSO deliveries—such as hull fabrication, topside module construction, and partial integration. These contributions, while not always reflected in full-unit delivery counts, are critical in building technical expertise and expanding industrial capabilities.

FLNG Construction

🇰🇷 South Korea South Korea continues to dominate FLNG, leveraging advanced integration capabilities and heavy-lift infrastructure,

Samsung Heavy Industries (SHI) delivering three major units and having another three under construction: Prelude FLNG (2017, Shell), PFLNG Dua (2020, Petronas), Coral Sul FLNG (2022, Eni). Ongoing projects include Cedar FLNG, Coral Norte FLNG, and ZFLNG.

Hanwha Ocean has delivered PFLNG Satu (2016, Petronas) .

🇨🇳 China China has delivered two FLNG units—but is actively expanding:

Wison Offshore & Marine has delivered Caribbean FLNG (2017), now Tango FLNG with Eni, NGUYA FLNG (2025) for Eni, and is building Genting FLNG. Wison is emerging as a powerhouse in the FLNG segment, particularly in modular and nearshore solutions.

CIMC is converting the FLNG Mark II for Golar (Fuji FLNG), marking a significant step forward in China’s offshore gas capabilities.

Despite facing sanctions and limited experience, Chinese yards are gaining traction in the FLNG space, especially for modular and nearshore solutions.

FPU Construction

Floating Production Units (FPUs) share many similarities with FPSOs but are typically deployed for gas fields without storage capability. Both Korea and China are active in this segment.

🇰🇷 South Korea

Samsung Heavy Industries (SHI): Argos FPU (2021, BP),

Hanwha: JIC FPU (ongoing, Chevron)

Hyundai Heavy Industries: Moho Nord FPU (2016, TotalEnergies), Shanandoah FPU (2025, Beacon Offshore Energy), Trion PFU (ongoing, Woodside)

🇨🇳 China

Wison Offshore & Marine: Ongoing Sakarya Phase 3 FPU (TPAO)

CIMC delivered Scarabeo 5 (2025, Eni)

COOEC delivered Lingshui 17-2 (2021, CNOOC)

FSO Construction

Floating Storage and Offloading units (FSOs) complement FPSOs by providing flexible storage solutions offshore. China’s yards are building:

COSCO Qidong: FSO Chalchi (ongoing, SBM/Woodside).

Nantong Strongwind: FSO Block B (ongoing, Petrovietnam)

In summary

South Korea continues to set the standard in FLNG, driven by engineering excellence, deep-water integration quays, and heavy-lift capabilities that enable one-lift topside installation. This leadership reflects decades of experience and strong relationships with global energy majors.

Meanwhile, China is diversifying aggressively—adding FPSO, FLNG, FPU, and FSO projects to its portfolio—and investing in modular construction strategies to accelerate schedules and reduce costs. Cosco Group’s multi-yard approach (Qidong, Dalian, Shanghai) positions it as a rising force, capable of handling complex FPSO integrations and expanding into new segments. Combined with Wison and CIMC’s push in FLNG and FPU, China is signaling a clear ambition to become a full-spectrum offshore construction powerhouse, challenging Korea’s dominance and reshaping the competitive landscape for large-scale floating production units.

Continue the reading on the following article at this link that will focus on infrastructures.